%20(1).avif)

The Cusp

Europe– the fallen king of infrastructure

From water- to highways, infrastructure used to be made by, in and for Europe. Yet, since the advent of the digital age the continent has fallen behind. Other geographies provide today’s core technologies – from Cloud to Mobile. The resulting civilizational dependence requires a strong remedy. Europe must find it in the renewed self-provision of key infrastructures – digital ones, this time.

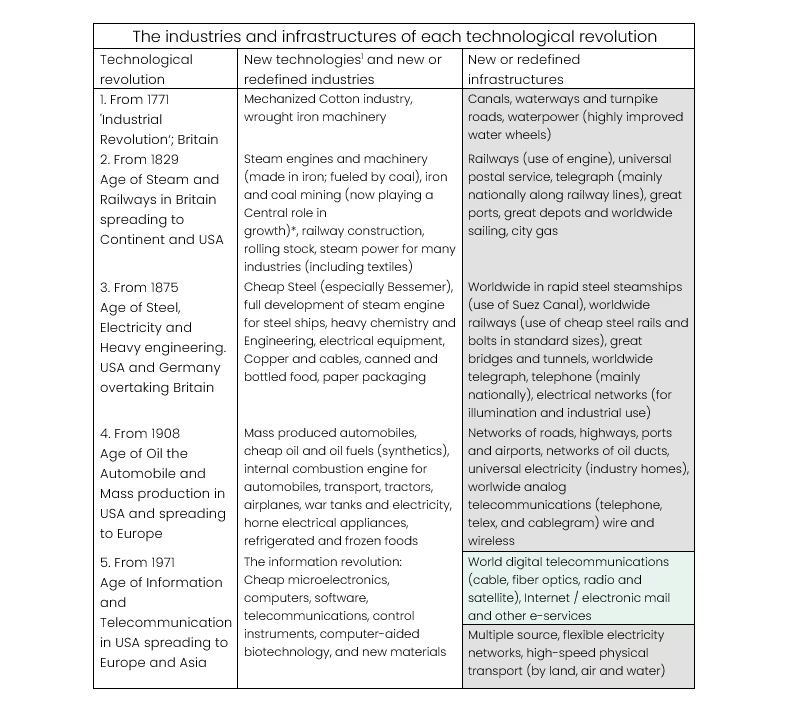

The birthplace of the Industrial Revolution, Europe, has provided its own infrastructure – and the world’s – since 1771: European steam engines, trains and cars have driven on European rail - and highways. Electricity and analog telecommunications networks (be they wired or wireless) have been developed by and for Europe.

The age of digital IT, spawned by the invention of the microprocessor in 1971 and of TCP/IP in 1983, broke this continuity. The new infrastructures it brought were no longer European. To illustrate the gravity of this rift, the following table lists the four technological revolutions and the infrastructures they have refined or defined. Highlighted in grey are those Europe has provided by and for itself. Highlighted in green – and framed – are those it has not.

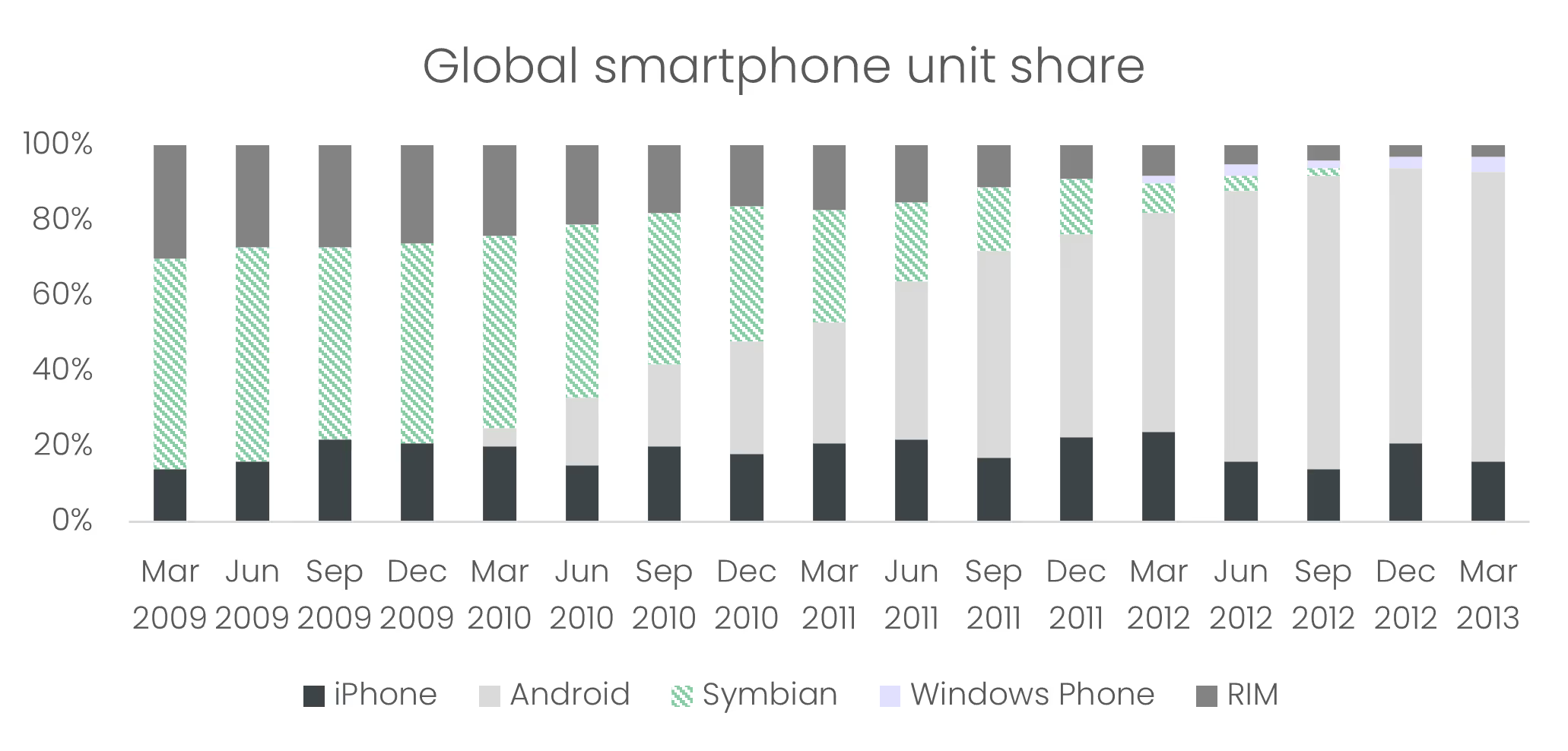

Zooming into the framed green we find that Europe has not invented nor provided the critical infrastructure of personal computers, and its mobile phones have been wiped out by smartphones. The following graphic depicts the market share of smartphone operating systems. Nokia’s Symbian – the only European contender in the pack – was dominant in the late 2000s. But then Android ate its lunch.

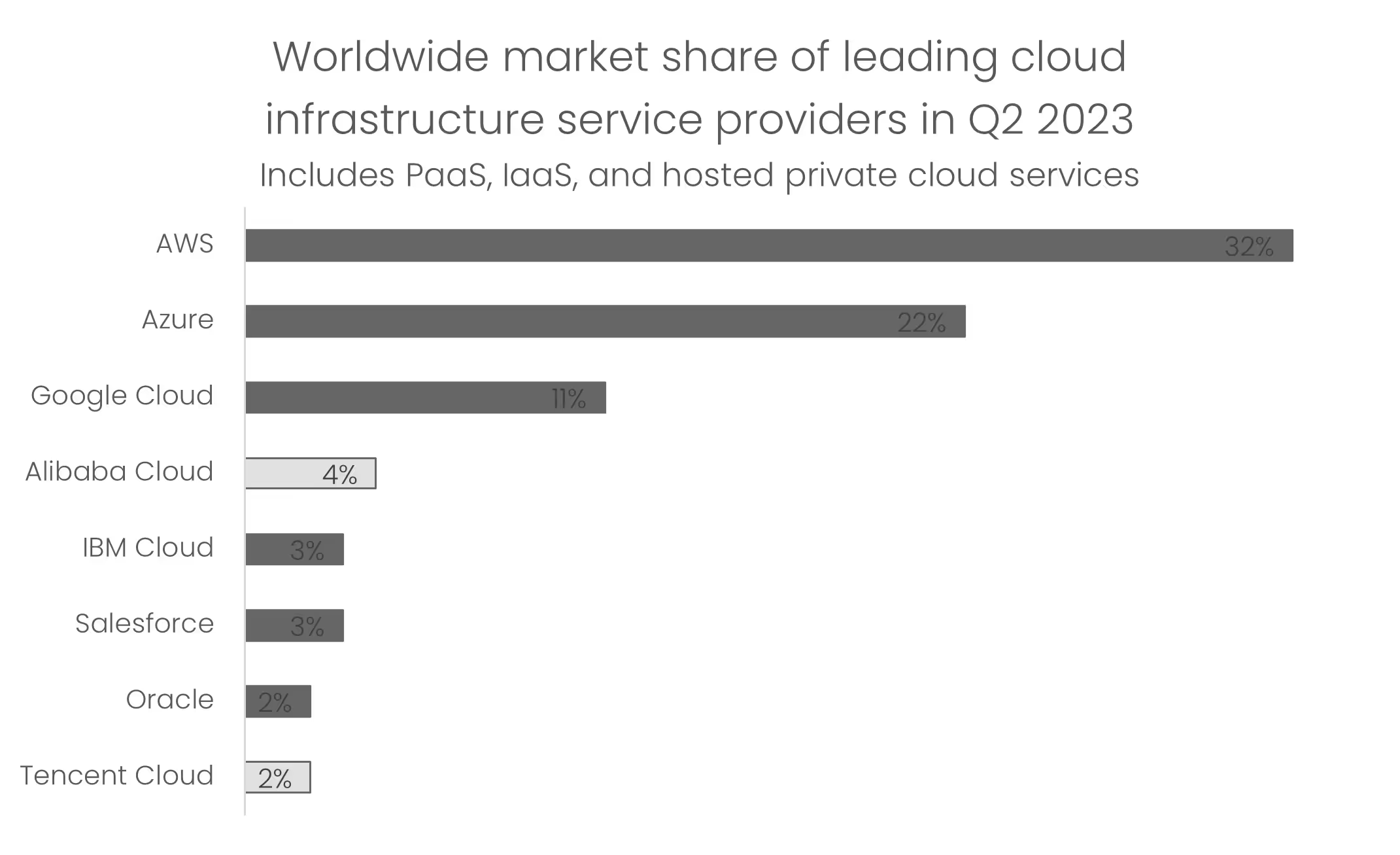

Cloud computing, too, has grown into a completely non-European realm. As the following graphic shows, none of the leading cloud infrastructure service providers in Q2 2023 were European.

Infrastructure impotence equals disaster. For it means dependence – economically, militarily and societally. Naturally, this dependence matters more when it concerns larger and more dynamic parts of the economy. And this is why the European self-provisioning of digital infrastructures is such a priority. As software is devouring the world, digital infrastructures are becoming primary. In the heydays of automotive liberty, we wouldn’t have wanted a foreign power to control the access to our highways – and have full information on all goods and people traversing them. In the world of bits and bites the rails and actors are of different name and form – but our preference remains the same.

Europe is on the cusp of leading infrastructure software

Europe is about to resume its leadership infrastructure provisioning. Aspiring creators of foundational systems face complex challenges in engineering and sales. Open Source (OSS) promises to remediate both by channeling Europe’s world class talent most creatively – and effectively. When Europe is on the cusp of its OSS trajectory – as it is – the region is on the cusp of leading infrastructure software.

Fortunately, a grim future of total dependence is unlikely. We believe Europe can and will build the digital infrastructures of the future. The continent already possesses powerful pockets of talent and research. It only needs to direct them.

Open Source is most potent way to structure infrastructure software

Infrastructure possesses two characteristics that render its creation an uphill battle for nascent companies.

First, to build an infrastructure product one must tackle tough problems that typically end in market failures. As offspring and enabler of novel general-purpose technologies (GPTs), infrastructure itself must be highly innovative2,3. In addition, infrastructure is a horizontal replacement for parts of a vertically integrated monolith and as such must be highly interoperable with those parts of the monolith that do remain. To complicate matters further, infrastructure as a mission-critical backbone possesses little to no fault tolerance.

Resolving the many challenges of infrastructure development requires tremendous amounts of capital – be it human or monetary. This huge, fixed cost is an investment affordable to none but the largest players. Even worse for nascent players, software benefits from huge economies of scale. Both dynamics intermesh to push for natural monopolies. Many infrastructures are provided by governments or large private entities.4

Second, selling an infrastructure product means selling a mission-critical backbone and installing it with an open-heart surgery. Young companies face questions of quality and endurance, e.g. with respect to funding. Bigger players, in contrast, can resort to their institutional brand. For a long time, nobody got fired for buying IBM.

Open Source software (OSS) remediates infrastructure’s two anti-competitive characteristics. Under this paradigm smaller companies (read startups) can tackle infrastructure problems – and play on (or above) the level of big tech companies. OSS can shift the power from capital to talent.

First, OSS creates a perfect market for innovation that let it productize infrastructure without market failures. OSS lowers the barriers to entry and scale by acquiring and coordinating resources creatively. The key: incentives, information and inclusion. In OSS, world-class technical talent leaves the hamster-wheel of capitalism to collaborate – not to earn hundreds of thousands of Euros at Big Tech, but for the esteem of their peers (network effect), to give back (gift economy), to learn, to meet great people and for the sheer, intrinsic pleasure of solving tough problems (homo ludens).5 Anyone can start an experiment and rally the best minds with nothing but the attractiveness of their technological innovation. For information is near perfect as the source code is public; and actors as coders are near perfectly rational. Projects without promise can fail fast and be supplanted – or reborn – by better alternatives. Finally, OSS collaborators are plentiful and often include potential customers. Tight, high-value feedback loops ensure unparalleled product-market fit and build the trust with buyers that is so necessary for selling critical components. Products are marketed to customers – developers – exactly how they like it: as code. Once the Trojan Horse of a free Open Source core has galloped into the gates, the purchase of closed-source features follows as a natural land-and-expand.

Second, OSS infrastructure begets further OSS infrastructure. Developers don’t reinvent the wheel when building new products and infrastructure is no exception. Consequently, if the infrastructures built upon – or components used – in a project are themselves OSS, the barriers to build and scale new infrastructure fall further. The result: more OSS infrastructure – now and in the future.

Finally, the interoperability and open standards typical of OSS mean that infrastructures can be developed in parallel – and build on each other. Experiments can become part of other experiments; a single one of them does not have to scale massively for their combined force to equal a substantial piece of infrastructure.

Of course, closed source solutions, too, can jump the challenges of building and selling infrastructure products. Teams with tight founder-market fit can achieve tight product-market fit. Winners may themselves possess proximity to the GPTs they are building infrastructure for (and may have pushed the GPTs themselves in previous roles). Further, closed-source solutions can crack the thick-skinned nut of selling mission-critical tools via a land and expand strategy. First, they find new killer features in the periphery and make them the new core. From here, they expand to replace old core infrastructure. Remedies against natural monopolists also exist outside of the open realm. Most directly, newcomers can themselves raise massive amounts of capital. They can leverage lower costs of living via geographical arbitrage. Or they can achieve breakthroughs so foundational that infrastructure costs plummet to levels impossible for previous paradigms.

Europe is on the OSS cusp

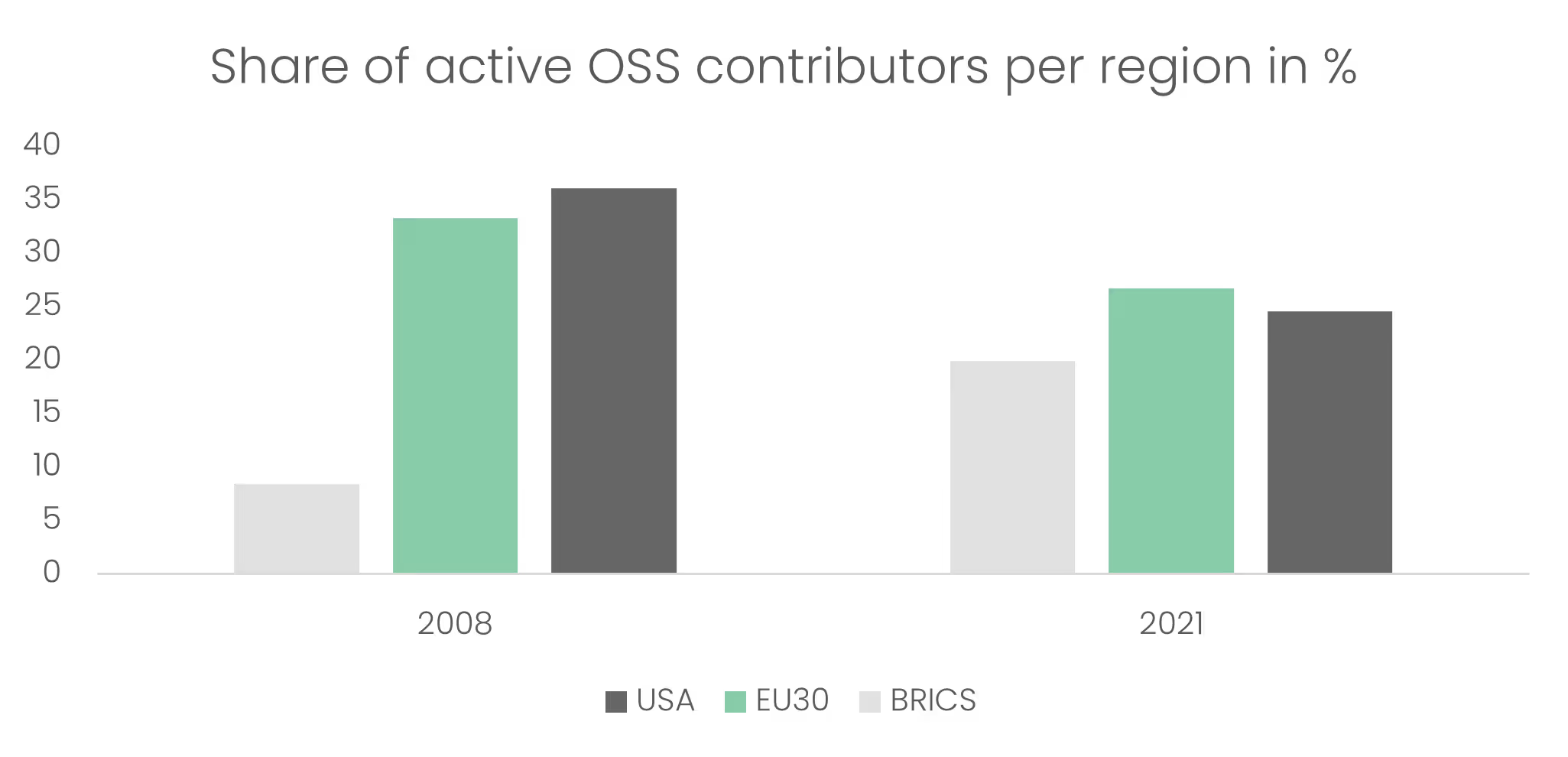

When it comes to OSS, Europe is on the cusp. The Eu30 built on a strong position in 2008 to surpass the United States in the number of active OSS contributors by 2021.

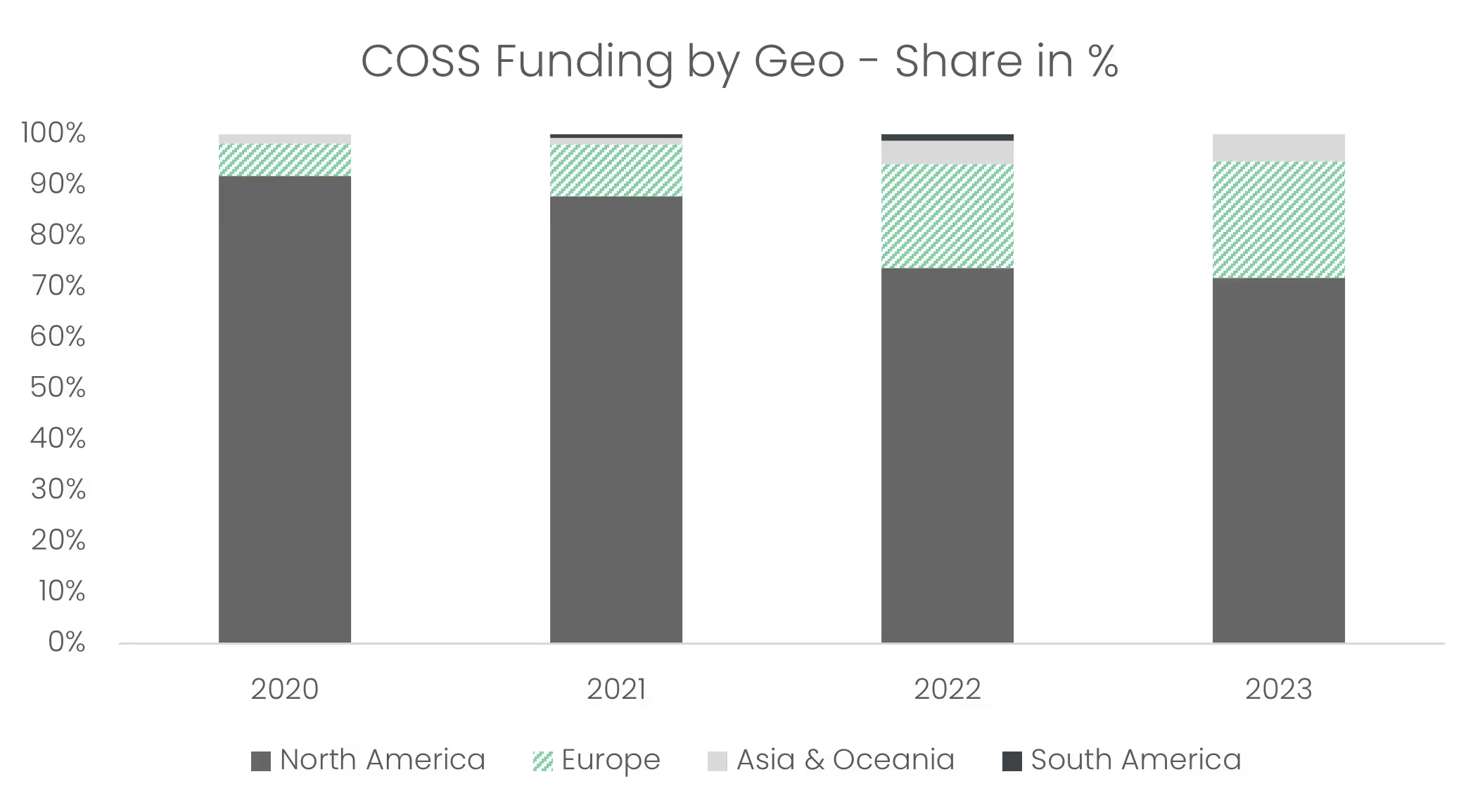

The OSS inflection point is most visible in venture funding directed to commercial Open Source (COSS) companies. Since 2020, Europe has grown its absolute volumes significantly – leading to an ever-larger relative share vs other leading geographies.

Europe’s foundations are strong

Contributors are the lifeblood of Open Source. For OSS projects can only be as excellent as the brains behind them. Europe may not have its own big-tech-colored buckets of capital, but it certainly has strong stables of world-class tech talent. On the cusp of OSS, the continent is on the cusp of providing global digital infrastructures.

Europe’s talent base is strong and talent migration trends are positive

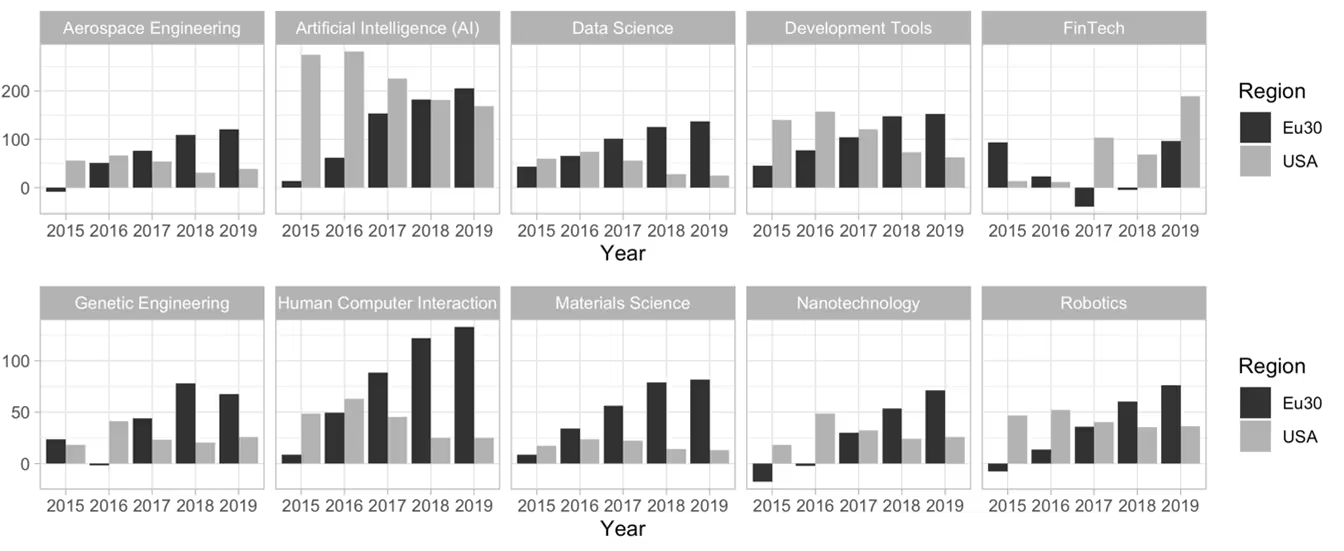

Europe’s pool of tech skills is leading globally. For “Disruptive Tech Skills” (World Bank and Linkedin August 2020) the Eu30 (EU27 + United Kingdom + Norway + Switzerland) already are on levels similar to those of the United States. The following figure lists the number of LinkedIn search results (Linkedin October 2023) that match said skills in said geographies. The Eu30 outperforms or equals the United States for Robotics, Nanotechnology, Material Science, Human Computer Interaction, Genetic Engineering, Fintech and Artificial Intelligence. The United States outperforms for Development Tools – and vastly outranks for Data Science and Aerospace Engineering.

One of the reasons for Europe’s strong skill position is that the continent keeps the top talent its top universities produce. In the realm of AI, leading European Undergraduates become leading European Graduates and Post-graduates:

Source: Marcopolo – NeurIPS 2019 paper submitters by education via Moasic Ventures (2020).

In addition, Europe is catching up across the board – thanks to skill migration. In the five years preceding Covid, for all dimensions but Fintech, the Eu30 received not only positive, but increasingly positive Net Change in Talent Migration (y-axis in graphic below).6

The United States, in contrast, saw its positive Net Change in Talent Migration decline for said dimensions and time periods.

The Eu30’s talent migration trends are positive

The observed patterns could point to a shift in the tides of talent migration – in favor of Europe. Earlier, between 2000-2010, Fink and Miguelez (2013) found a slightly negative inventor net migration for the Eu30 – which compared quite poorly to a very positive U.S. position. Even back then, though, the picture was nuanced. On the level of individual regions, some European regions outperformed (Caviggioli et al. 2020). From 2005-2010 Zuidoost-Noord-Brabant in the Netherlands and Zurich in Switzerland beat the United States’ San Jose-San Francisco-Oakland and Boston-Worcester-Manchester metropolitan areas both in growth and level of migrants’ PCT patents while Stockholm and Milano did so in growth (Ibid.).

Europe’s research is world-class

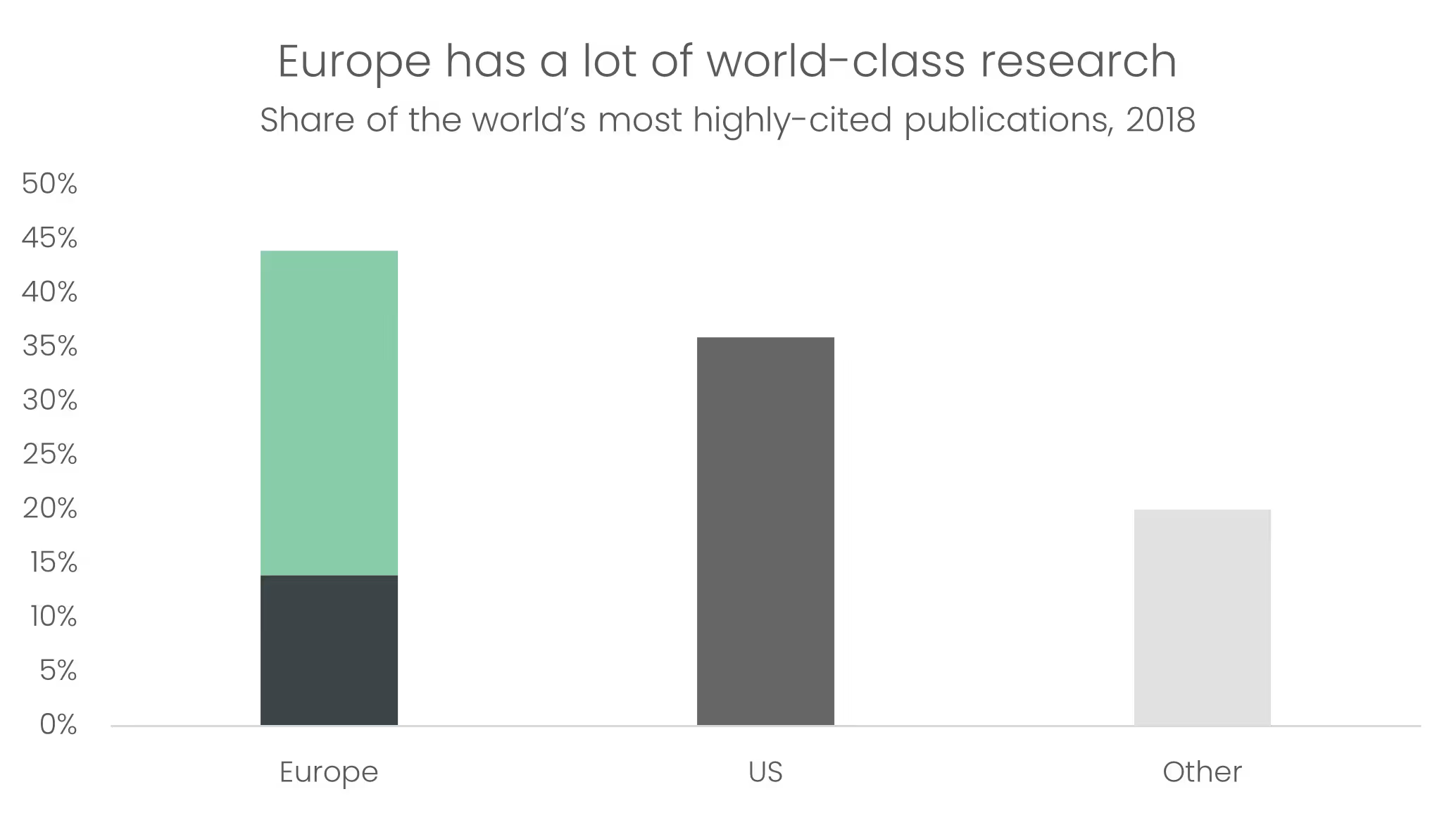

The story of European talent is one of global leadership in quantity – and quality. Europe’s research is excellent. Its share in the world’s most highly cited publications surpasses the United States’ and China’s by a substantial margin.

The Opportunity

In praise of infrastructure

Infrastructure rocks via its close relationship with general purpose technology. New GPTs require new infrastructures. The number – and opportunity - of GPT-specific infrastructures is vast and follows a tilted-croissant trajectory. For digital infrastructures, the best is yet to come.

Infrastructure, or the building beneath, is an ingenious invention. For it not only facilitates but catalyzes innovation.

First, Infrastructure combines horizontal specialization with interoperability to allow for vertical disintegration – and more horizontal specialization. Put simply, if all the technological world is an onion, higher layers don’t have to reinvent the wheel every time and build all lower layers in-house. Rather, they can rely on infrastructure providers and focus on their comparative, higher-level advantages. Applications, for example, can be developed without having to rewire transistors – in high-level languages rather than binary.

A second catalytic feature of infrastructure is its durable versatility. The most potent kinds of infrastructure can serve as inputs to many applications – not just one. And they remain intact after use, are not consumed.

The infrastructure deck is stacked

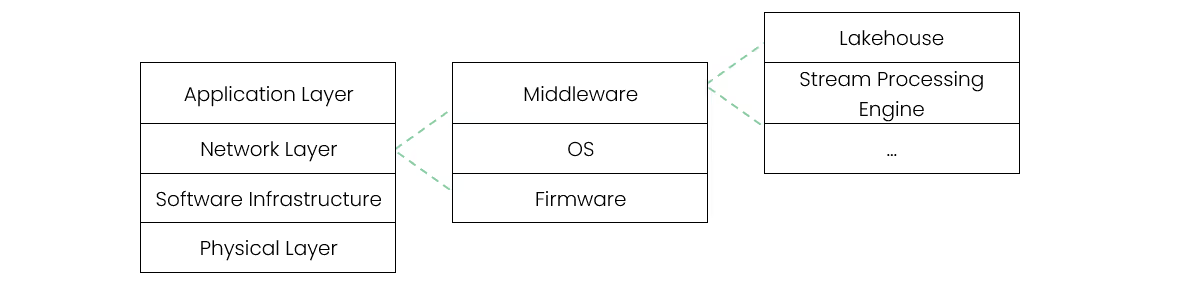

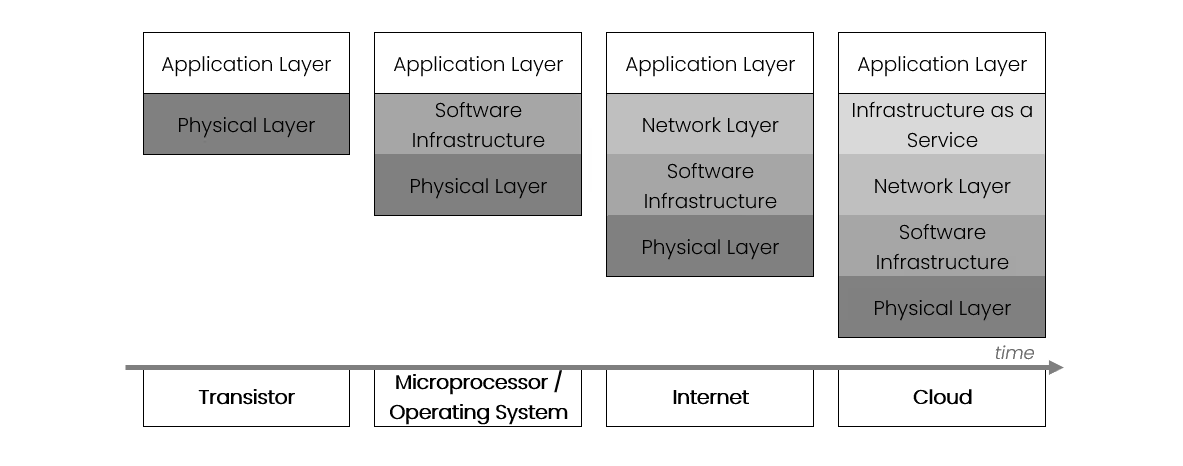

In the context of software, the infrastructure stack looks as follows:

Each infrastructure layer itself can consist of several sub-layers of infrastructure, which, in turn consist of sub-layers:

The future builds beneath

The opportunity for new software structure layers is as boundless as the number of GPTs within Information Technology. New general purpose technologies require new infrastructures – if they are to avoid the straight jacket of eternal vertical integration. And even mature general purpose technologies see their infrastructure layers evolve – because of further disruptive innovation within certain layers, differentiation within individual layers, or synergistic consolidation of adjacent layers.

To illustrate, let’s dive into the infrastructure lifecycle of one general purpose technology. As the following graph indicates, a new general purpose technology (e.g. robotics) typically starts fully vertically integrated. In the beginning, it can rely on no GPT-specific infrastructure layers – and only build on top of the infrastructure layers of the GPTs that came before it.

Establishing the first GPT-specific infrastructure layers takes time, as it is initially expensive to ready the market. Yet, as soon as their foundation is laid, the number of GPT-specific infrastructure layers quickly proliferates. That is, until the point at which individual layers have become commoditized and become bundled again to achieve synergies in integration. Graphed, then, the number of GPT-specific infrastructure layers follows a tilted-croissant trajectory:

The following graphic applies the tilted croissant to the evolution of the software stack. In the beginning, there was the transistor, and the transistor was with the physical layer, and the physical layer was good. Writing a new application required rewiring transistors – until the first programmable microprocessor spawned the first software infrastructure – and operating systems expanded upon it. The internet then established the network layer. Most recently, Cloud found a further abstraction to build upon in Infrastructure as a Service.

Topics and geography

The digital infrastructure opportunity is as varied as it is vast. We prioritize by stack position, GPT nature, and OSS density. Ceteris paribus, more opportunity exists in lower levels, more unique GPTs, and geographies with a higher local share of OSS contributors.

Topically, we identify areas of infrastructure promise based on three core principles. First, the more low-level the software layer, the higher the opportunity. Lower-level infrastructures are the basis for higher level infrastructures. As such they enable everything that comes on top. Hardware is hard as it comes with iteration troubles, high upfront investment, long feedback cycles, and arduous procurement – to name a few. Second, the more general purpose a technology the more it is and the more it sparks infrastructure. And third, the more unique a technology’s data, processing or execution, the more it needs tailored infrastructure. Importantly, some verticals don’t just require specific applications, but tailored infrastructure layers as well. Such is the case if the data, processing, or execution they govern cannot be sufficiently served by generalists. Integration with adjacent systems, for example, will require vertical-specificity – especially if adjacent systems are highly regulated (e.g. banks) or legacy (e.g. hospitals).

Geographically, some areas boast more dense OSS communities than others. Norway, Sweden, and Finland host particular penetration. So do Germany, Switzerland, the Netherlands and the United Kingdom.

Europe has always been a leader in infrastructure provision. United by Open Source the continent’s world-class talent and research will extend this truth to the digital realm. At Cusp Capital we look forward to working with the ambitious European companies building digital infrastructures for the world.

1 Perez’s technological revolutions differ from General Purpose Technologies (GPTs, see definition in footnotes below). They are GPTs, but most GPTs are smaller in scope.

2 As versatile innovations with broad applications (and lasting impact), GPTs drive complementary advancements in various fields and catapult entire economies into new strata. Key examples include broad breakthroughs such as the steam engine – but also more specific advancements such as the mobile phone.

3 Infrastructure is itself a GPT as lower levels of the tech stack enable their more elevated counterparts. This facet of infrastructure is essential. Armed with Occam’s Razor we must still restrict its discussion to this footnote. In the context of this text infrastructure for GPT sits in the driving seat – while infrastructure as GPT rides shotgun.

4 In another market failure, infrastructure enables future innovation but itself cannot fully participate in this additional value-creation. Infrastructure’s positive externality leads to its under-provision by strictly profit-maximizing capitalists.

5 About 50% of contributions to OSS projects are volunteer work (Riehle et al. 2014). Of course, capitalist incentives continue to exist in the form of professional networking and resume building. Cases of Big Tech opening closed source projects may also follow growth and profit paradigms; but the dynamics they unleash in the OSS projects themselves remain highly non-monetary.

6 Net Change in Talent Migration is defined as “The net gain or loss of members from another country with a given skill divided by the number of LinkedIn members with that skill in the target (or selected) country, multiplied by 10,000” (World Bank and Linkedin August 2020B). We calculated the Eu30 number as a simple average of the group’s countries. Net Change in Talent Migration normalizes for different sizes in skill populations. As these populations are similar in the Eu30 and USA we can also infer absolute, non-normalized changes with strong confidence.

.jpg)

.jpg)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)